FATF Recommendations – RAHN CASE STUDY ISSUE NO.19-2022

How Anti-Money Laundering (AML) and Counter Terrorist and Proliferation Financing (CTPF) laws have greatly affected banking

Rahn Consolidated’s articles and case studies are aimed at socialising, climatising, creating awareness. Cautioning economic participants regarding economic crime schemes and Proliferation Financing. The focus will be on anti-money laundering. The investigations around economic crime scheme risks, reporting, and most importantly, its regulatory compliance. The term “Economic crime schemes” is often used interchangeably with “Financial Crime”.

Issue No.19 focuses on aspects contained in the Financial Action Task Force (FATF) Mutual Evaluation Recommendations and Immediate Outcomes (IOs). Which affect all Financial Institutions. We have seen how Anti-Money Laundering (AML) and Counter Terrorist and Proliferation Financing (CTPF) laws have greatly affected banking, insurance, and financial institutions. There are certainly greater risks of non-compliance at this stage. It is vital to get your business compliant as soon as possible to avoid potential regulatory fines.

In this issue, we will focus on cases affecting Proliferation Financing as part of Immediate Outcome 4 (IO4). South African Accountable Institutions must know which countries are regarded as high-risk . When it comes to Proliferation Financing and start embedding controls to ensure that they curb these risks.

Financial Action Task Force Recommendations: A case study on industry impact of Immediate Outcome 4: Preventative Measures on Proliferation Financing (Broader Africa)

Enjoy the Read!

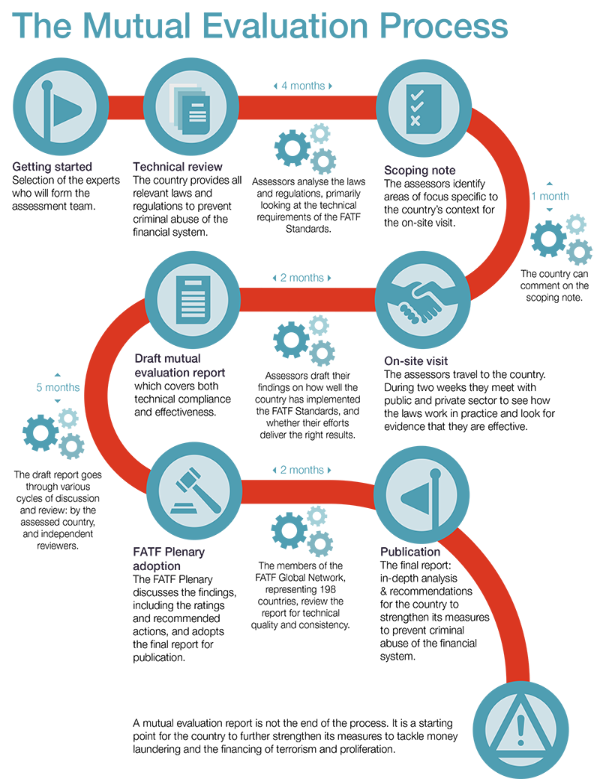

Mutual Evaluation Report (MER) Immediate Outcome 4 (IO4): Preventative Measures

The FATF MER Immediate Outcomes apply to the following financial institutions:

- Large banks from a material and risk perspective;

- The securities sector (Financial Service Providers and Collective Investment Schemes managers) mostly from a material perspective;

- High-risk sectors: estate agents, attorneys, and casinos.

- Several Financial Institutions are not subject to all the AML/CFT obligations which impact the effectiveness of preventive measures. The legislation has however been evolving to ensure that all Financial Institutions have the same robust controls to curb AML/CFT.

One of the outcomes, emanating from the FATF MER, is that since April 2019 South Africa has implemented Targeted Financial Sanctions (TFS) for Proliferation Financing well, most of the time without delay, but some major improvements are needed, as the private sector’s understanding is uneven, and supervision of Proliferation

Financing related obligations is new. For this reason, the next upcoming desktop reviews by the FIC (followed by Onsite Inspections) will be on the effective embedment of Proliferation Financing measures which should go hand in hand with your currently embedded processes and capabilities on Terrorist Financing

and Sanctions. Rahn Consolidated can assist in the embedment of all these capabilities and in ensuring that there is a single view across all these respective areas. Having said that, in understanding Proliferation Financing, one needs to expand on what it is and how to curb it in your business.

“Proliferation is defined by the Financial Action Task Force (FATF) as the illegal manufacture, acquisition development, export, trans-shipment, brokering, transport, transfer, stockpiling, or use of nuclear, chemical, or biological weapons and their means of delivery and related materials.”

Prohibitions against Financial Institutions

Below are financial prohibitions against which Financial Institutions should be guarding (in this example North Korea, officially known as the Democratic People’s Republic of Korea (DPRK), is the focus point):

Controls on financial institutions : Financial institutions are prohibited from maintaining relationships, including correspondent banking relationships, with DPRK financial institutions

Controls on vessels and aircraft : Leasing or chartering vessels, aircraft, or crew services to/from DPRK is prohibited

Prohibitions on financial support : Includes granting of export credits, guarantees, or insurance

From a FATF perspective, the below recommendations relate to proliferation financing:

- Recommendation 1: Requires countries to identify, assess, and understand their Proliferation Financing risks, take commensurate action to mitigate these risks, and require Financial Institutions to do the same.

- Recommendation 2: Requires effective national cooperation and coordination mechanisms to combat Proliferation Financing.

- Recommendation 7: Requires implementation of United Nations Security Council Resolution Terrorist Financing Sanctions on Proliferation Financing (i.e., asset freezes).

Proliferation Financing Case Study

Although there are not many proliferation case studies in South Africa, the most prominent case in Africa, which showed why North Korea is set at high risk when it comes to proliferation financing, emanates from the Democratic Republic of Congo (DRC).

Background

- Congo Aconde was registered as a company by two North Koreans (Pak Hwa Song and Hwang KilSu) in 2018 in the DRC;

- They facilitated construction projects for the DRC Government in three provinces from 2018 to late 2019;

- They further engaged in activities that appear to violate UN, EU, and US sanctions which include but are not limited to:

- Opening bank accounts at Afriland First Bank for their company;

- Undertook construction projects in the DRC by erecting statues, a type of construction activity explicitly forbidden by the UN sanctions.

- The Congolese government funds reportedly served to pay for the statues.

Act of falsification: this is where conducting Customer Due Diligence is prominent

- The Congolese provided the North Koreans with passports during the company formation process;

- The passports indicated they are “Ministry of Foreign Affairs” employees;

- They were in the DRC for official government business;

- The Nationality was therefore recorded as ‘Korea’ or ‘Korean’;

- Congo Aconde, therefore, listed a residential address on incorporation records.

Acts of Proliferation Financing:

- There were US Dollar bank accounts opened at Afriland First Bank in the name of Congo Aconde, that maintained a corresponding relationship with other Banks, which lead to the opportunity to conduct US Dollar transactions without restriction;

- The Bank indicated the account of Congo Aconde received $407,800 in deposits and approximately $408,145 in withdrawals. It was further indicated that these transactions were in cash and not electronic transfers, which shows the importance of establishing Cash Transaction Reporting capabilities embedded in the business.

- And finally, the Bank indicated no incoming or outgoing international transfers which then, in turn, meant that the MLRO did not submit an International Fund Transfer Report. This implies domestic funding through Congolese funds or bulk cash transfers.

As part of AML/CTPF capabilities Rahn Consolidated provides, it assists organisations to build systems to conduct client identification and verification and further screen individuals and institutions against among other sanctions, terrorist, and proliferation lists.

Ref: The Sentry

Van Vuuren Street

Mulberry Gardens

Constantia Kloof

Johannesburg

1709

Tel: +27 87 802 1384